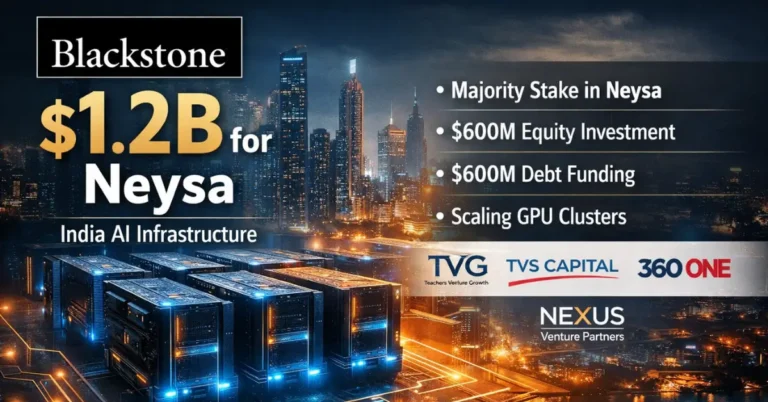

Blackstone’s $1.2B Neysa deal accelerates India AI infrastructure

The financing underscores how fast India’s AI infrastructure market is maturing—and how capital, policy, and enterprise demand are converging to localize GPU capacity at scale.

Deal details and strategic fit

Blackstone will take a majority stake in Neysa through up to $600 million in primary equity, alongside Teachers’ Venture Growth, TVS Capital, 360 ONE Asset, and Nexus Venture Partners; the company also plans up to $600 million in debt to accelerate buildout. The raise is a step change from Neysa’s earlier $50 million and positions the Mumbai-headquartered startup to scale domestic GPU clusters for enterprises, public sector agencies, and AI developers. The move aligns with Blackstone’s broader data center and AI infrastructure strategy—following stakes in QTS and AirTrunk, and specialized AI providers such as CoreWeave (U.S.) and Firmus (Australia)—and adds a dedicated India platform to that portfolio.

Market drivers: GPU supply, data localization, and latency

Global AI demand continues to outstrip supply of advanced accelerators and suitable data center capacity, creating a window for “neo-clouds” that deliver dedicated GPUs, transparent pricing, and faster time-to-capacity than hyperscalers. India’s installed base remains nascent—industry estimates put it below 60,000 GPUs—but is expected to scale into the low millions within a few years as use cases harden. Multiple forces are at play: data-residency obligations in regulated sectors, the need to cut inference latency for India-based users, growing activity from domestic AI labs, and national programs to catalyze indigenous compute (including initiatives under the IndiaAI Mission). The result is a clear market opening for providers that can stand up sovereign-aligned, GPU-first infrastructure with enterprise-grade SLAs.

How Neysa positions in India’s neo-cloud GPU stack

Neysa is building a customized, GPU-centric cloud that emphasizes local control, fast onboarding, and operational support tailored to enterprise and government buyers.

GPU-first clusters with enterprise-grade SLAs and security

Neysa operates roughly 1,200 GPUs today and plans to ramp beyond 20,000 over time, with management indicating demand could more than triple capacity in the next year—potentially within nine months if current deals close. Capital will fund large-scale clusters spanning compute, high-performance networking, and storage, while a portion goes to software for orchestration, observability, and security. The operating model focuses on white-glove support, tight response SLAs, and customization that many customers say they struggle to obtain from generalized hyperscale environments. For AI builders, this translates into faster access to accelerators and the ability to fine-tune or serve models in-region; for CIOs, it offers compliance-ready environments with clearer workload isolation and cost controls.

Target customers: regulated enterprises, public sector, AI labs

Immediate demand is coming from financial services, healthcare, and government workloads that require data locality and auditable controls, as well as AI labs that need predictable training and inference capacity close to end users. Global providers with large India user bases are also evaluating in-country deployments to meet latency targets and data-handling requirements. Neysa’s pitch is a domestic platform that combines dedicated capacity with services tuned to Indian regulatory expectations and procurement processes.

What this means for telcos and enterprise IT buyers

The buildout of sovereign-aligned GPU clouds in India will reshape network, data center, and procurement strategies across telco and enterprise ecosystems.

5G edge integration and network monetization

For operators, localized AI clusters create new opportunities to colocate GPU resources near 5G cores and metro edge sites to serve latency-sensitive applications: computer vision, industrial automation, network analytics, and RAN optimization. Expect tighter integration between GPU clouds and multi-access edge computing (MEC), with premium interconnects, deterministic latency guarantees, and slice-aware routing. Fiber backhaul, peering, and metro dark fiber will become gating factors for AI service performance—and potential revenue levers for telcos and ISPs.

Design priorities: power, cooling, interconnects, and security

AI racks are pushing 30–60 kW densities and will increasingly require liquid cooling and high-efficiency power distribution. Network architects should plan for low-jitter, lossless fabrics—InfiniBand or Ethernet with RoCE—and storage designs that sustain GPU throughput (e.g., NVMe over Fabrics). Security must be built-in: strong tenant isolation, confidential computing, and continuous posture management. Facilities strategy will hinge on power availability, renewable PPAs, and water-use constraints, as sustainability targets tighten and tariffs evolve.

Procurement strategy: capacity reservations and diversification

GPU allocation remains the choke point. Buyers should secure capacity early, weigh reserved versus on-demand economics, and model preemption risks. To reduce vendor concentration, consider a balanced approach across local neo-clouds, hyperscalers’ India regions, and on-prem clusters—abstracted by portable MLOps stacks to avoid lock-in. Evaluate accelerator diversity (where viable) and ensure transparency on SLAs, incident response, and replacement policies for failed GPUs to protect training timelines.

India AI compute competitive landscape

India’s AI compute race will feature a mix of domestic specialists, hyperscalers, and data center operators converging through partnerships and M&A.

Convergence of hyperscalers and domestic data center operators

AWS, Microsoft Azure, and Google Cloud continue to expand India regions and edge footprints, while domestic data center platforms—such as STT GDC India, Nxtra by Airtel, Jio’s data center ventures, AdaniConneX, Sify, and Yotta—are scaling capacity and power. Specialized providers are likely to partner with carriers for last-mile performance, with private equity-backed platforms (including Blackstone’s portfolio) pursuing cross-region synergies. Expect tighter coupling between GPU clouds and carrier networks, including private connectivity, secure on-ramps, and integrated observability.

Policy signals and emerging AI standards

The Digital Personal Data Protection Act and IndiaAI programs are steering demand toward in-country compute and responsible AI practices. Watch for incentives on domestic capacity, import duties on accelerators, grid and renewable policies, and reporting requirements on energy and water use. On the technical front, harmonization around model governance, auditability, and secure data exchange will influence how enterprises choose between sovereign, public, and hybrid AI deployments.

Action plan for CIOs, telcos, and AI builders

With capital flowing and capacity coming online, decisions made in the next two to four quarters will set AI infrastructure baselines for the next five years.

Guidance for CIOs and CTOs

Map workloads by data sensitivity and latency, then align each to the right landing zone: neo-cloud for regulated and predictable GPU needs, hyperscale for elastic bursts, on-prem for crown jewels. Reserve capacity for 2026–2027 programs now, and standardize on portable toolchains for orchestration, observability, and security. Build FinOps guardrails for GPU consumption, and lock down data governance and lineage to ease audits.

Guidance for telecom operators and ISPs

Productize low-latency connectivity into GPU clouds with deterministic SLAs, peering, and MEC integration. Prioritize metro builds where AI demand clusters—financial hubs, healthcare corridors, manufacturing zones—and bundle network, edge colocation, and managed security. Explore joint offers with neo-clouds targeting enterprise AI and network analytics workloads.

Guidance for AI builders

Benchmark model training and inference on domestic capacity to quantify latency and data-handling gains, and design for hybrid placement across regions. Use capacity reservations for production-critical training, and deploy inference close to users to cut costs and improve UX. Incorporate robust observability and rollback paths to manage model drift and compliance.

Bottom line: Blackstone’s investment validates India’s shift from AI pilot projects to scaled, sovereign-grade infrastructure—and signals that buyers who lock in capacity, interconnects, and governance now will move faster as the next wave of AI workloads lands.