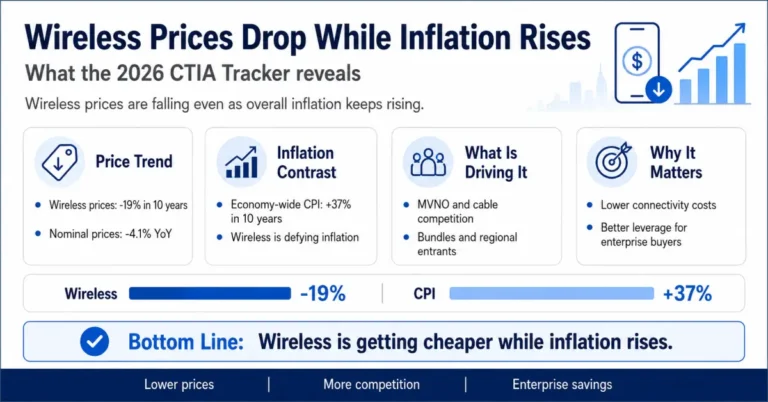

Wireless Prices Are Falling While Everything Else Rises: A Strategic Market Signal

While most sectors of the U.S. economy continue to grapple with persistent inflationary pressure, wireless services are moving in the opposite direction — and the implications extend well beyond the consumer market.

CTIA 2026 Tracker Data: Wireless Deflation in an Inflationary Economy

CTIA’s newly released More for Less: 2026 Wireless Affordability Tracker offers a striking data point: nominal wireless prices have declined 4.1% over the past year and 19% over the past decade, according to the Bureau of Labor Statistics’ Consumer Price Index. Adjusted for inflation, postpaid unlimited plans are down roughly 10% year-over-year and nearly 35% compared to five years ago. Prepaid options have seen even steeper compression — falling more than 50% over the same five-year window, driven in large part by an explosion in plan diversity, with the tracker identifying more than a thousand distinct offerings currently available to U.S. consumers.

Put this in context against the broader economy: the economy-wide CPI rose 2.7% last year and more than 37% over the past decade. Wireless is not just holding steady — it is actively defying the macro trend. Compare it to other household expenditures: college tuition is up 1.5% year-over-year, rent up 2.9%, cable TV up 3.7%, and gas and utilities up 10.8%. Wireless stands alone as a category delivering measurable deflation in an inflationary environment.

How Declining Wireless Costs Are Expanding Household Spending Power

The CTIA report frames wireless affordability as an economic offset — a sector that effectively subsidizes consumers’ ability to spend elsewhere. Cellular services now represent just 1.73% of average American household spending, according to the BLS Consumer Expenditure Surveys. That figure sits well below housing at 33.44%, transportation at 16.96%, food at 12.85%, and healthcare at 7.89%. For enterprise decision-makers evaluating total cost of connectivity — whether for mobile workforce enablement, IoT deployments, or distributed edge infrastructure — this pricing trajectory represents a favorable structural condition.

Why Wireless Prices Keep Falling: MVNO and Cable Competition Explained

The affordability gains documented in the tracker are not accidental — they reflect deliberate competitive strategy from both incumbent carriers and a growing wave of MVNO and cable-backed entrants reshaping the market’s pricing floor.

Xfinity Mobile, Optimum, and MVNOs Are Aggressively Lowering the Pricing Floor

The cable industry’s wireless push is accelerating. Comcast‘s Xfinity Mobile recently introduced two new tiers — Mobile Plus at $45 per line and Mobile Select at $30 per line — expanding its competitive footprint in the mid-market. Meanwhile, Optimum, operating as an MVNO on T-Mobile‘s network infrastructure, launched its “UnBig Your Bill” retail campaign, explicitly positioning against AT&T and Verizon pricing and backing the offer with a $150 gift card guarantee where price matching wasn’t possible. These moves signal that cable-backed wireless players are no longer content to compete at the margins — they are pursuing aggressive share capture with price as the primary weapon.

Regional Broadband Providers Like Midco Are Bundling Wireless to Compress Prices Further

Beyond the national and cable players, regional broadband operators are now bundling wireless into their service stacks. Midco’s recent launch of Midco Mobile is a notable example — offering a by-the-gig Flex plan at $15 per month and an unlimited tier at $30, designed to complement its existing fiber internet, MidcoTV, and landline portfolio. This bundling strategy reflects a broader industry pattern: operators are using wireless as a retention and cross-sell tool within converged service bundles, compressing standalone wireless pricing in the process.

Enterprise Wireless Strategy: What the Pricing Decline Means for IT and Procurement Leaders

For telecom executives, enterprise IT leaders, and network strategists, the declining cost curve in wireless is more than a consumer story — it carries direct operational and competitive relevance.

Why Enterprises Should Benchmark Wireless Contracts Against Today’s Market Rates

As wireless prices trend downward while performance — driven by 5G network densification, spectrum deployment, and network slicing capabilities — continues to improve, the cost-per-bit economics for enterprise mobile connectivity are becoming increasingly favorable. Organizations managing large mobile workforces, field operations, or IoT device fleets should be revisiting their connectivity contracts and benchmarking against current market rates. The gap between legacy enterprise agreements and current market pricing may be material.

How MVNO Growth Is Creating New Leverage for Enterprise Connectivity Buyers

The proliferation of MVNO entrants — many backed by T-Mobile, AT&T, or Verizon wholesale agreements — is also expanding the ecosystem of potential connectivity partners for enterprise buyers. As operators like Optimum and regional players like Midco demonstrate, wireless is increasingly being delivered as a component within broader managed service bundles. For CTOs and procurement leaders, this creates new leverage points in vendor negotiations and opens pathways to multi-service agreements that can drive down blended connectivity costs.

Spectrum Policy, Merger Review, and the Regulatory Signals Behind Wireless Deflation

The sustained price decline documented by CTIA also has policy dimensions worth monitoring. A market delivering consistent deflation in a high-inflation environment is one that regulators and lawmakers will point to as evidence that competition is functioning — which has implications for spectrum policy, merger review, and infrastructure investment incentives. Network strategists should factor this regulatory posture into their long-range planning, particularly as 5G Advanced and early 6G standardization discussions begin to shape the next investment cycle.

Wireless Is Getting Cheaper and Faster Simultaneously — Here Is What Industry Stakeholders Should Do Next

Wireless pricing is doing something almost nothing else in the U.S. economy is doing right now — it is getting cheaper, faster, and more feature-rich simultaneously. For consumers, that is a tangible relief valve against broader inflation. For industry stakeholders, it is a signal that competitive intensity in the wireless market is structurally elevated and unlikely to ease. Operators that are not actively managing their pricing architecture, bundle strategy, and MVNO positioning risk ceding ground to more agile entrants who are already treating price as a primary growth lever. The CTIA tracker is not just a consumer advocacy document — it is a competitive intelligence asset.