India’s 6 GHz spectrum battle intensifies, with global device/cloud ecosystems pushing for unlicensed Wi-Fi while operators lobby for IMT licensing to support national 5G capacity growth.

6G spectrum planning accelerates, as GSMA warns mid-band decisions over the next two years will define the performance ceiling for 6G through the 2030s in dense urban markets.

5G differentiation emerges, with Ericsson’s Mobility Report showing operators commercializing guaranteed latency, uplink boosts, and application-aware prioritization — moving beyond “speed-only” plans.

India’s 5G base set to exceed 1B users by 2031, marking one of the fastest 5G scale curves globally, driven by modernization, ARPU repair, and broad device adoption.

FCC advances major upper C-band auctions, setting the stage for a 2027 reallocation that could unlock up to 180 MHz for 5G/6G capacity and reshape satellite incumbency.

Airbus expands mission-critical broadband with Agnet Direct, ensuring secure operations when private or commercial 4G/5G coverage is impaired — validated on France’s RRF.

Jio bundles 18-month Google Gemini Pro access for all 5G users, signaling AI as a core monetization lever for emerging-market operators.

Nokia outlines its AI-native 6G strategy, concentrating R&D on AI-driven RAN, cloud-native core evolution, and next-generation radio systems.

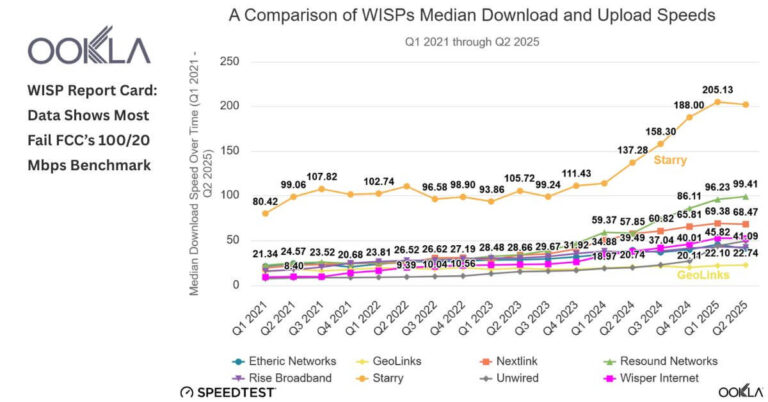

WISPs vs Starlink: performance gap narrows, with U.S. WISPs accelerating speeds even as LEO satellite networks strengthen rural competitiveness.

CTIA Catalyst impact surpasses 30M people, one of the most effective mobile-first public benefit deployments in the U.S.

Orange readies Europe’s first commercial NTN D2D SMS, extending coverage to satellite zones for messaging and location sharing.

AT&T activates 3.45 GHz nationwide, upgrading 23,000 sites with new mid-band spectrum to accelerate 5G FWA and mobile capacity.

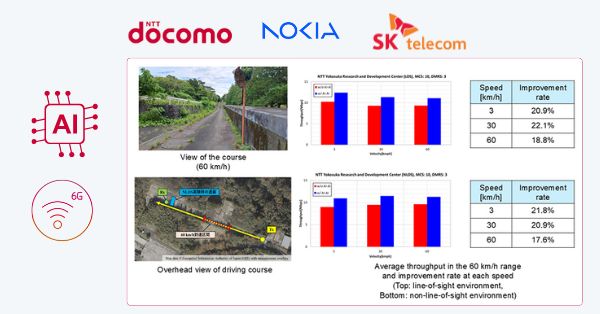

NTT Docomo, Nokia Bell Labs & SK Telecom double 6G throughput with an AI-AI air interface — a real-world outdoor milestone toward AI-native RAN.

Airtel’s credit upgrade reflects ARPU expansion, deleveraging, and sustained 5G subscriber growth in India.

T-Mobile showcases 5G slicing at the Las Vegas Grand Prix, integrating private 5G and edge video into broadcast and public-safety workflows under extreme density.

UK tribunal clears handset overcharging class action, targeting Vodafone, EE, O2, and Three for post-contract device pricing practices.

Jio pushes for flexible 5G net-neutrality rules, emphasizing slicing-enabled QoS for URLLC, industrial automation, cloud gaming, and premium video.

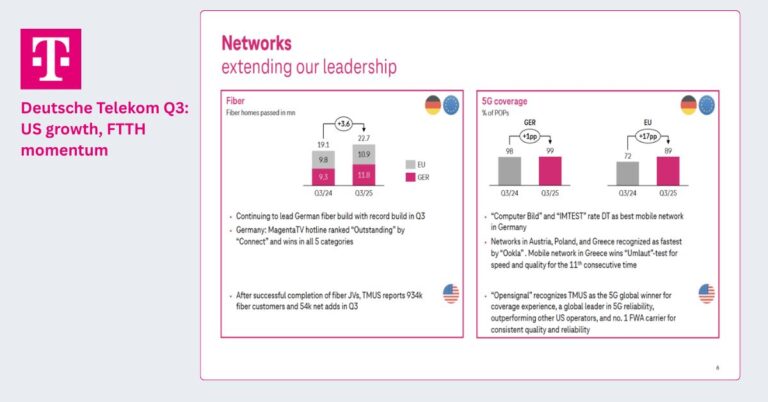

Deutsche Telekom reports strong Q3, with U.S. momentum, FTTH expansion, and raised full-year guidance.

Amazon rebrands Project Kuiper as Amazon Leo, signaling readiness for commercial LEO broadband targeting enterprise and consumer markets.

VC4 highlights “invisible infrastructure” losses, detailing how undocumented fibers, circuits, and legacy assets drain operator revenue and opex.

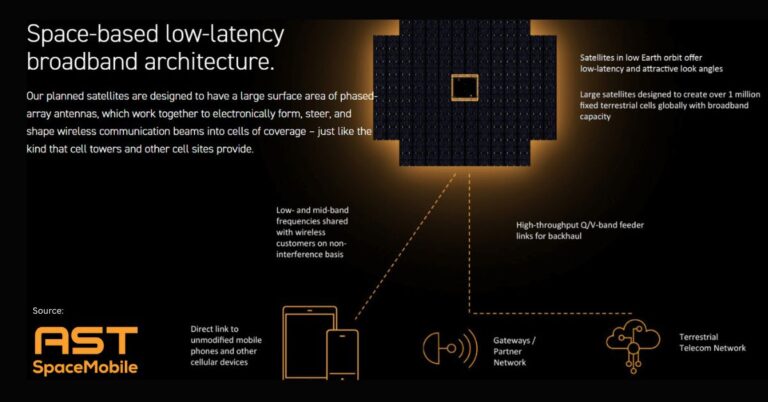

AST SpaceMobile targets early 2026 nationwide D2D coverage, progressing toward continuous service later in the year with major operator partners.

Spain validates upper 6 GHz (n104) for 5G-Advanced, marking the last major mid-band candidate for 5G/6G capacity expansion.

Ericsson deploys neutral-host 5G at 10 World Trade, setting a scalable model for multi-operator indoor coverage in commercial real estate.

Jio refreshes prepaid plans with AI, OTT, and differentiated 5G bundles — signaling a shift from pure connectivity to value-added service packaging.

Nokia to modernize Denmark’s TNN network, extending its role as sole 5G RAN supplier with AI-driven RAN automation and energy-efficient upgrades.

Nokia & LMT advance tactical 5G for Baltic defense, integrating secure 5G radio with military-grade systems for coalition operations.

Ookla launches Speedtest Pulse Wi-Fi Analyzer, addressing in-building performance issues that drive churn and truck rolls across fiber, FWA, and LEO deployments.

Vodafone & AST SpaceMobile propose a sovereign NTN model for Europe, delivering D2D satellite broadband under national operational frameworks.

BT & Starlink partner on rural ultrafast broadband, offering satellite-powered home connectivity where fixed-line expansion faces terrain and cost barriers.

BT accelerates job cuts as Openreach faces broadband subscriber pressure and increased market competition.

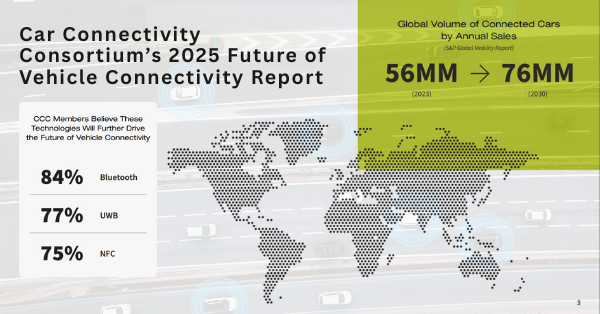

CCC outlines BLE, UWB & NFC standards for connected vehicles, defining the next phase of secure, interoperable vehicle connectivity.

Telecom prices continue falling, posing margin pressure even as operators invest heavily in fiber, 5G, and cloud networks.

Broadband Forum releases 5G FWA for MDUs spec, enabling one outdoor mmWave CPE to deliver gigabit broadband across entire apartments using existing wiring.

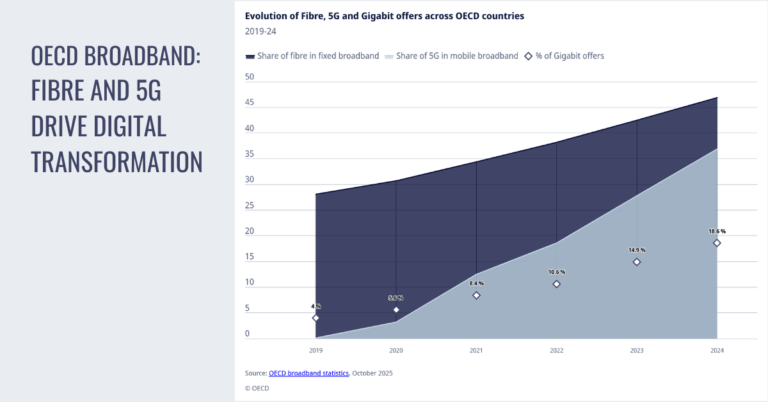

OECD data confirms fiber & 5G as global transformation engines, as markets shift from build-out to scaled digital infrastructure.

Dutch telcos launch CAMARA fraud APIs nationwide, aligning with GSMA Open Gateway for network-powered security services.

TELUS Digital takeover strengthens AI CX & 5G monetization, consolidating SaaS and automation capabilities under a single operating model.

FCC moves to rescind CALEA cybersecurity mandate, resetting expectations after high-profile intrusion reports.

Vodafone selects Dell for scaled Open RAN rollouts across Europe, advancing automated, cloud-aligned 5G modernization.

O2 integrates Starlink direct-to-cell for UK rural coverage, launching messaging and low-bandwidth data first.