- Tech News & Insight

- May 13, 2026

- Hema Kadia

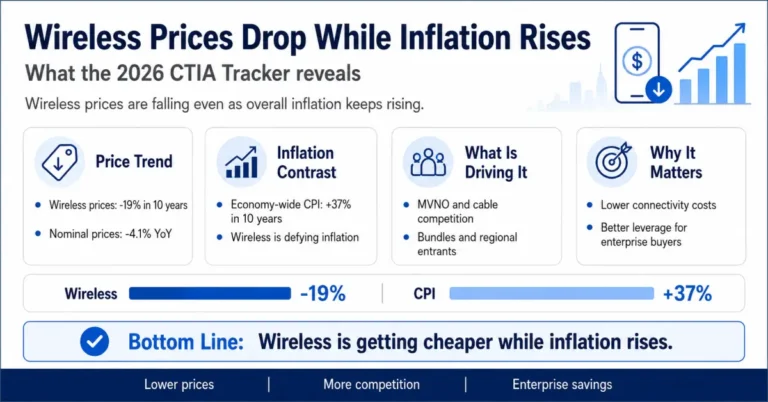

Wireless services are defying U.S. inflation trends in a way virtually no other sector is. According to CTIA's newly released More for Less: 2026 Wireless Affordability Tracker, nominal wireless prices have declined 4.1% over the past year and 19% over the past decade, while the economy-wide CPI rose more than 37% over the same period. Adjusted for inflation, postpaid unlimited plans are down roughly 10% year-over-year, and prepaid options have fallen more than 50% over five years. For enterprise decision-makers, this pricing trajectory represents a structurally favorable condition for mobile workforce and IoT connectivity planning.