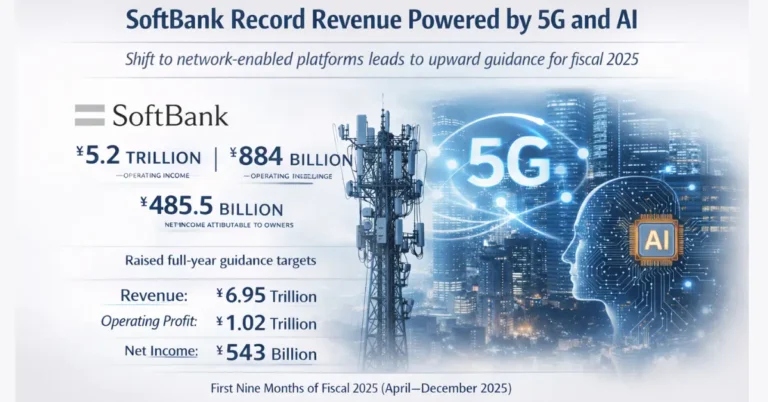

SoftBank Corp. delivered its strongest nine-month performance on record and lifted full-year guidance, underscoring a strategic shift from connectivity-only services to network-enabled platforms in AI, cloud, and edge. Through the first nine months of fiscal 2025 (April–December 2025), SoftBank reported revenue of ¥5.2 trillion, up 8% year over year, and operating income of ¥884 billion, also up 8%, with net income attributable to owners rising 11% to ¥485.5 billion. Management raised full-year targets to ¥6.95 trillion in revenue, ¥1.02 trillion in operating profit, and ¥543 billion in net income, signaling confidence heading into the March 31, 2026 year end.